Your credit score affects everything from loan approval to apartment applications, yet most people don't understand how it's calculated or how to improve it effectively.

The Five Factors

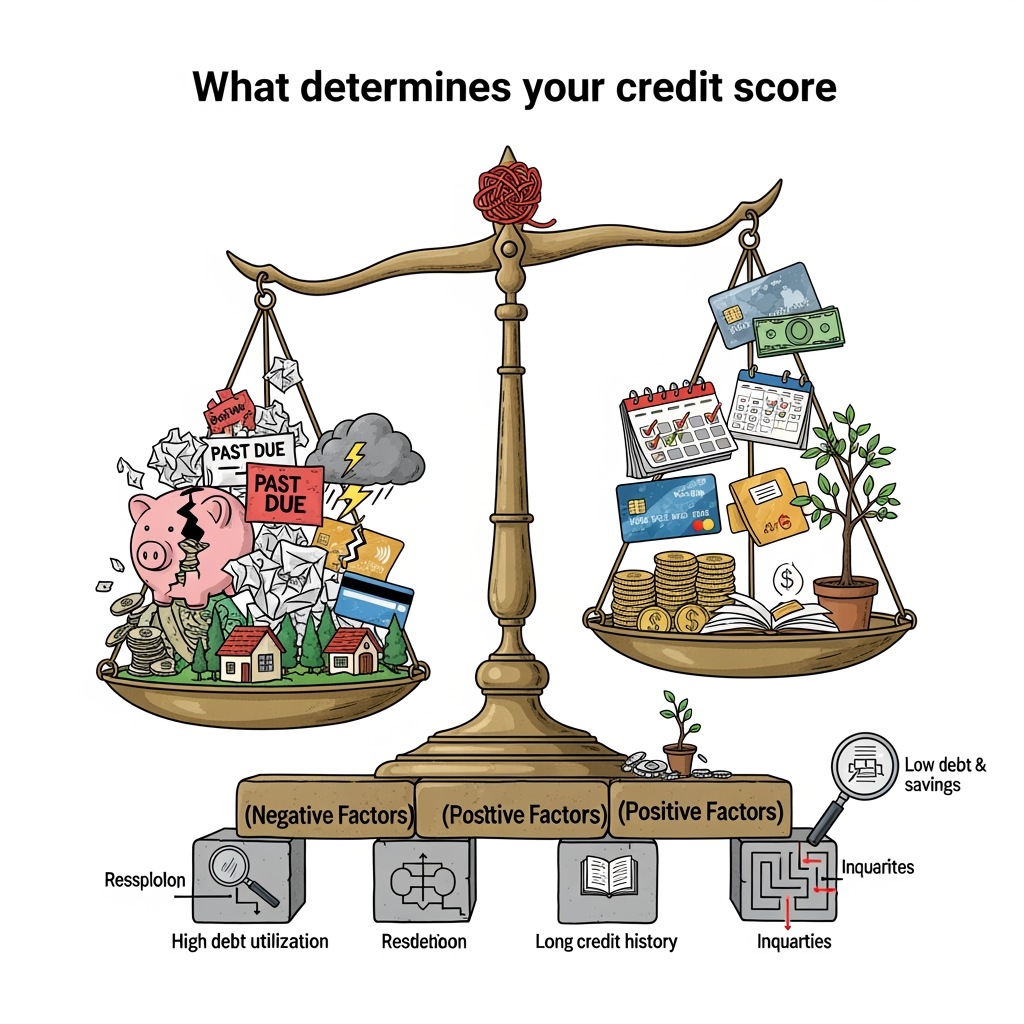

Payment history counts for 35% of your score. Even one late payment can drop your score significantly. Amounts owed make up 30%, measuring how much of your available credit you're using. Length of credit history contributes 15%, rewarding long-term accounts. Credit mix adds 10%, considering variety in account types. New credit rounds out the remaining 10%.

The Utilization Myth

Many believe carrying a small balance improves scores. This is false. Credit utilization—the percentage of available credit you're using—should stay below 30%, ideally under 10%. Paying off balances in full each month achieves the best results.

Hard vs Soft Inquiries

Checking your own credit creates a soft inquiry with no score impact. Applying for new credit triggers a hard inquiry, temporarily lowering your score. Multiple hard inquiries for the same loan type within 14-45 days typically count as one.

Building Credit From Nothing

Without credit history, you're essentially invisible to the system. Secured credit cards, becoming an authorized user on someone else's account, or credit-builder loans can establish initial history.

This article was generated by AI to provide informational content.